The 5-Account Wealth System Explained

Most people manage money the same way.

Income arrives in one account.

Bills get paid from that same account.

Savings, investments, and emergencies all compete for whatever remains.

At first glance it feels manageable. But over time this structure creates confusion. It becomes difficult to see what money is actually doing, where progress is happening, or whether wealth is truly being built.

One of the simplest ways to change this is to structure your personal finances the way a business owner structures cash flow.

Businesses rarely run everything through one account. They create purpose-driven accounts so every dollar has a clear role.

This is the idea behind the 5-Account Wealth System.

Instead of reacting to money as it arrives, you create a structure that directs it intentionally.

Why Structure Changes Everything

Most people believe financial success comes from two things:

earning more

or spending less.

Both matter. But something more fundamental sits underneath them.

Structure.

Without structure, even disciplined people struggle to maintain financial progress. Decisions become emotional, priorities shift, and money slowly drifts away from the goals it was meant to serve.

Structure removes friction. It replaces constant decision-making with a system that quietly guides your finances forward.

The result is clarity.

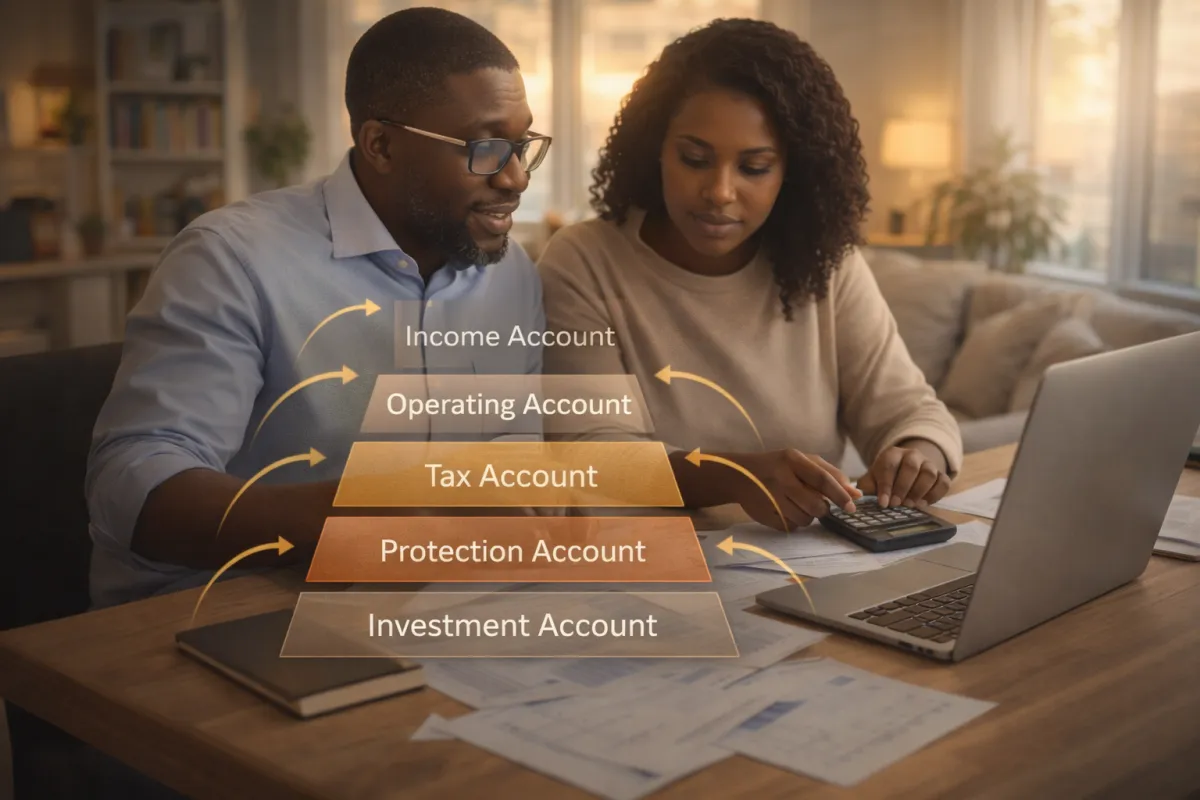

The Five Accounts

The 5-Account Wealth System organizes your finances into five roles that money plays in your life.

Each account exists for a specific purpose.

1. Income Account

Every dollar first arrives here.

Think of this account as the entry point of your financial system. It is not designed for spending. Instead, it serves as the clearing point where income gathers before being distributed intentionally.

Once income arrives, it is allocated across the other accounts according to your plan.

This step introduces something most households lack:

intentional cash flow management.

2. Operating Account

This is where daily life runs.

Rent or mortgage, groceries, transportation, utilities, and other core living expenses flow through this account.

Separating operating money from everything else creates visibility. You can clearly see what your life actually costs without mixing it with savings, taxes, or investments.

Importantly, fun money also comes from this account.

Entertainment, dining out, hobbies, travel spending, and other lifestyle choices are funded here. The key difference is that these expenses are planned rather than impulsive.

Fun is not the enemy of financial progress.

But fun must live inside a structure, not outside of it.

When fun money is clearly defined, people enjoy it without guilt and without undermining the rest of their financial plan.

3. Tax Account

For professionals, entrepreneurs, and high-income earners, taxes are often the most disruptive financial surprise.

The tax account removes that surprise.

A portion of income is automatically transferred here as soon as money arrives. This ensures tax obligations are funded consistently throughout the year rather than becoming a stressful lump-sum payment later.

Beyond the practical benefit, this account introduces something deeper:

financial responsibility and discipline.

Taxes stop being an afterthought and become a built-in part of the system.

4. Protection Account

Life rarely moves in a straight line.

Unexpected expenses, temporary income disruptions, or emergencies can quickly destabilize finances if no buffer exists.

The protection account houses resources designed to absorb shocks. It may include emergency reserves, short-term contingency funds, or liquidity designed to keep your financial life stable during uncertainty.

Its purpose is simple:

protect the foundation you are building.

Without protection, even strong financial progress can unravel quickly.

5. Investment Account

This is where wealth grows.

Instead of investing only when extra money appears, this account receives funds deliberately and consistently.

It may support:

investment portfolios

business opportunities

equity ownership

long-term asset growth

The shift here is psychological as much as financial.

Investing becomes systematic, not occasional.

Over time, this account represents the bridge between income and wealth.

The Emotional Dimension Most People Overlook

The benefits of a system like this are not only financial.

They are emotional.

When money has clear destinations, three silent pressures begin to disappear.

First, the anxiety of not knowing where your money went.

Second, the guilt of feeling like you should be doing better financially.

Third, the quiet fear that you may be falling behind.

Structure replaces chaos with clarity.

Money stops feeling unpredictable. It begins to feel directed.

And because fun money has a place within the system, financial discipline no longer feels like deprivation.

Designing Your Financial System

The goal of the 5-Account Wealth System is not complexity. It is intentionality.

Income flows in.

The system distributes it.

Your life runs smoothly, your obligations are covered, and your future is funded consistently.

Wealth rarely emerges from scattered effort.

More often, it grows from simple systems that quietly move money toward the life you are trying to build.

And sometimes the most powerful step you can take is simply giving every dollar a place to go.